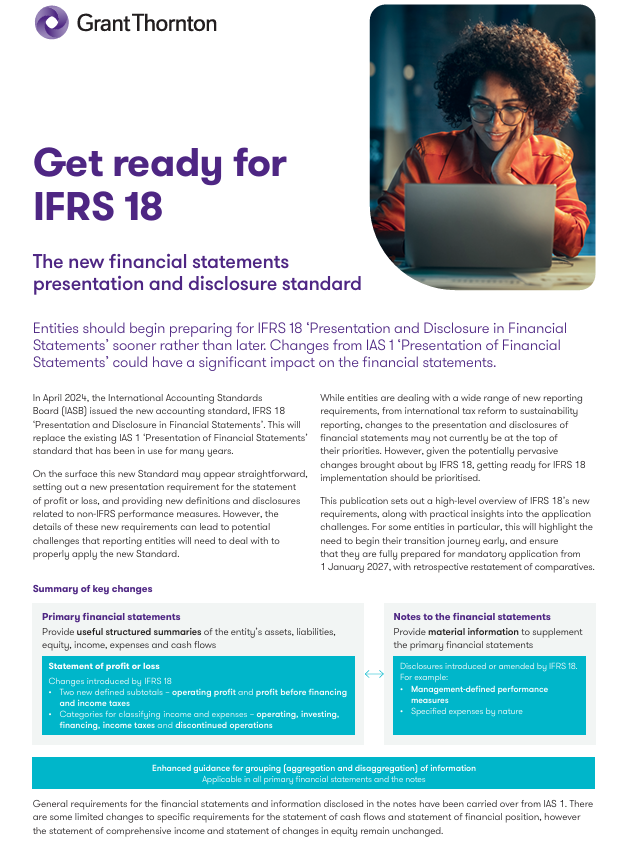

In April 2024, the International Accounting Standards Board (IASB) introduced IFRS 18: Presentation and Disclosure in Financial Statements, marking a significant shift from IAS 1. Effective for annual reporting periods starting 1 January 2027, IFRS 18 requires mandatory retrospective application, emphasising early preparation to ensure a seamless transition. We share below a high-level summary of the changes introduced, along with a detailed guide for your reference.

Contents

Key Highlights of IFRS 18

Statement of Profit or Loss:

- The introduction of two new subtotals: Operating profit or loss, Profit or loss before financing and income taxes.

- Income and expenses are classified into operating, investing, financing, income taxes, and discontinued operations.

Enhanced Disclosures:

- Focus on management-defined performance measures (MPMs), requiring detailed reconciliation and explanations.

- Guidance on aggregation and disaggregation to ensure financial statements provide helpful, structured summaries.

Updated Financial Statement Presentation:

- Operating expenses can now be presented using a hybrid approach of nature and function.

- Improved classification of income and expenses based on the underlying assets or liabilities, ensuring transparency.

Impact on Systems and Processes:

- Organisations may need to overhaul existing financial reporting systems to align with the new classification requirements.

- Early identification of alternative performance measures (APMs) that qualify as MPMs will ease compliance.

Transition Challenges:

- Restating comparative information from 1 January 2026.

- Integration of new requirements into interim financial statements for seamless reporting.

Alignment with Other Standards:

- Amendments to standards like IAS 7, IAS 8, and IAS 34 to support the transition.

Preparing for the Transition to IFRS 18

In April 2024, the International Accounting Standards Board (IASB) introduced IFRS 18: Presentation and Disclosure in Financial Statements, marking a significant shift from IAS 1. Effective for annual reporting periods starting 1 January 2027, IFRS 18 requires mandatory retrospective application, emphasising early preparation to ensure a seamless transition.